Entire life and universal life insurance are both considered long-term policies. That suggests they're designed to last your entire life and will not expire after a particular time period as long as needed premiums are paid. They both have the prospective to accumulate cash worth gradually that you may be able to obtain versus tax-free, for any reason. Since of this feature, premiums might be greater than term insurance coverage. Whole life insurance coverage policies have a set premium, suggesting you pay the same quantity each and every year for your coverage. Just like universal life insurance coverage, entire life has the possible to accumulate money value gradually, creating an amount that you might have the ability to borrow against.

Depending upon your policy's prospective money value, it may be used to avoid an exceptional payment, or be left alone with the prospective to collect value in time. Prospective development in a universal life policy will vary based on the specifics of your individual policy, in addition to other aspects. When you buy a policy, the issuing insurer develops a minimum interest crediting rate as described in your contract. However, if the insurance provider's portfolio earns more than the minimum rate of interest, the business may credit the excess interest to your policy. This is why universal life policies have the potential to earn more than a whole life policy some years, while in others they can make less.

Here's how: Given that there is a cash worth element, you may be able to avoid superior payments as long as the money value suffices to cover your required expenses for that month Some policies may enable you to increase or decrease the death benefit to match your particular situations ** Oftentimes you might borrow against the cash value that might have built up in the policy The interest that you may have earned in time accumulates tax-deferred Whole life policies provide you a fixed level premium that won't increase, the possible to accumulate cash value over time, and a repaired death benefit for the life of the policy.

As an outcome, universal life insurance premiums are normally lower during durations of high interest rates than whole life insurance premiums, typically for the very same quantity of coverage. Another essential difference would be how the interest is paid. While the interest paid on universal life insurance coverage is often adjusted monthly, interest on a whole life insurance coverage policy is normally adjusted annually. This might suggest that during durations of rising rates of interest, universal life insurance policy holders may see their cash values increase at a fast rate compared to those in entire life insurance coverage policies. Some people may prefer the set death advantage, level premiums, and the capacity for growth of a whole life policy.

Although whole and universal life policies have their own special functions and benefits, they both concentrate on offering your enjoyed ones with the cash they'll need when you pass away. By dealing with a certified life insurance agent or company agent, you'll have the ability to choose the policy that finest fulfills your private needs, spending plan, and monetary objectives. You can likewise get acomplimentary online term life quote now. * Supplied required premium payments are timely made. ** Increases may undergo extra underwriting. WEB.1468 (How much is renters insurance). 05.15.

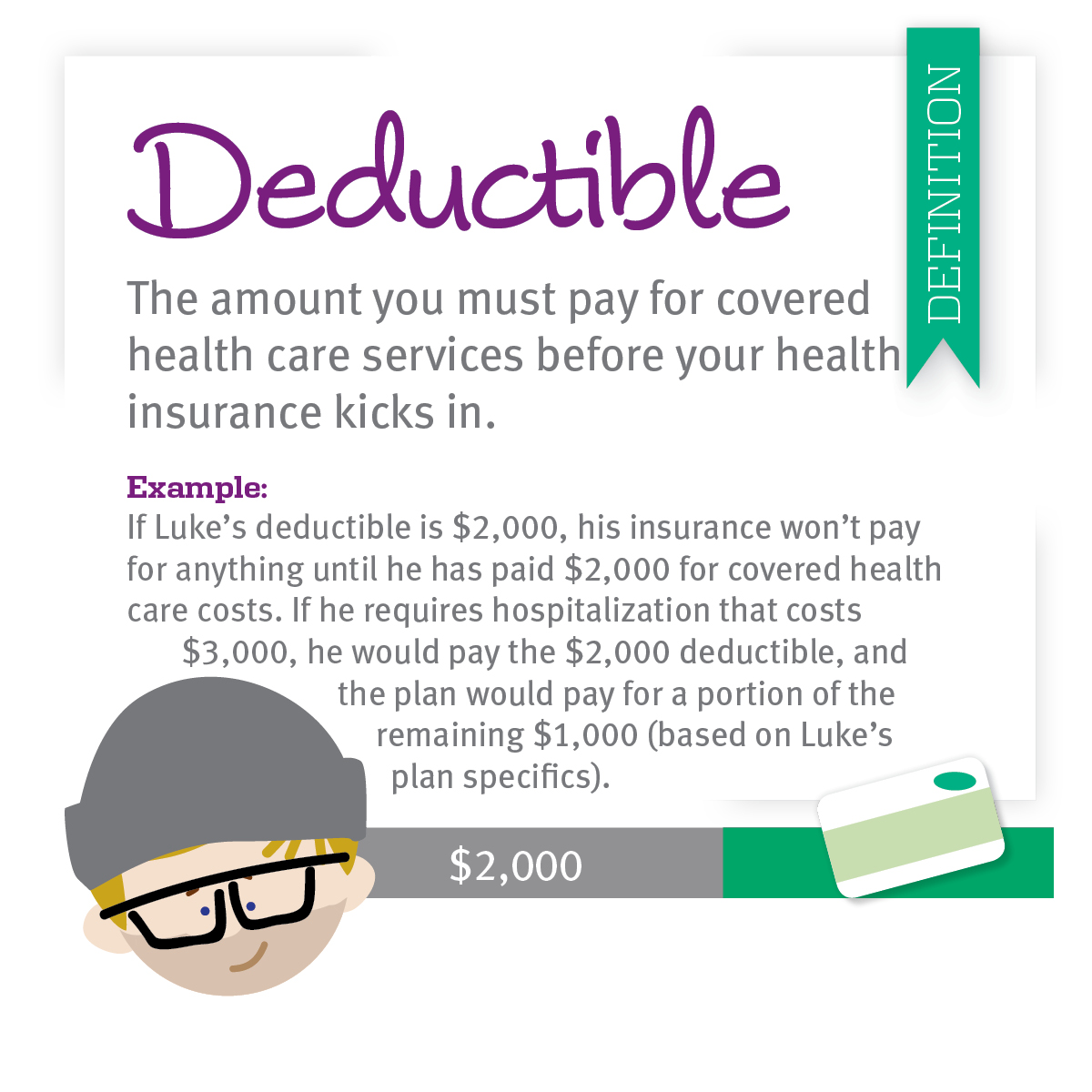

Indicators on How Much Is Insurance You Need To Know

You don't need to think if you need to enlist in a universal life policy since here you can find out everything about universal life insurance advantages and disadvantages. It's like getting a preview before you buy so you can decide if it's the right type of life insurance for you. Keep reading to discover the ups and downs of how universal life premium payments, cash value, and death benefit works. Universal life is an adjustable kind of permanent life insurance that enables you to make changes to two main parts of the policy: the premium and the survivor benefit, which in turn impacts the policy's cash worth.

Below are some of the overall advantages and disadvantages of universal life insurance. Pros Cons Created to provide more flexibility than entire life Does not have the ensured level premium that's offered with whole life Money worth grows at a variable interest rate, which might yield higher returns Variable rates also imply that the interest on the cash worth could be low More opportunity to increase the policy's cash value A policy usually requires to have a positive money worth to stay active One of the most appealing functions of universal life insurance is the ability to pick when and just how much premium you pay, as long as payments fulfill the minimum amount needed to keep the policy active and the IRS life insurance guidelines on the optimum amount of excess premium payments you can make (What is an insurance deductible).

But with this flexibility also comes some disadvantages. Let's review universal life insurance coverage advantages and disadvantages when it pertains to altering how you pay premiums. Unlike other types of irreversible life policies, universal life can adapt to fit your monetary requirements when your money circulation is up or when your budget is tight. You can: Pay higher premiums more regularly than needed Pay less premiums less often and even avoid payments Pay premiums out-of-pocket or use the cash worth to pay premiums Paying the minimum premium, less than the target premium, or skipping payments will adversely affect the policy's cash value.